Data centers are new factories of the 21st century

Inference is becoming the new intermediate good that powers almost all economic activity

Aside from the hype, ever wondered why there is so much money going into building data centers, setting an unprecedented pace of investment, and also sparking conflicts in local communities?

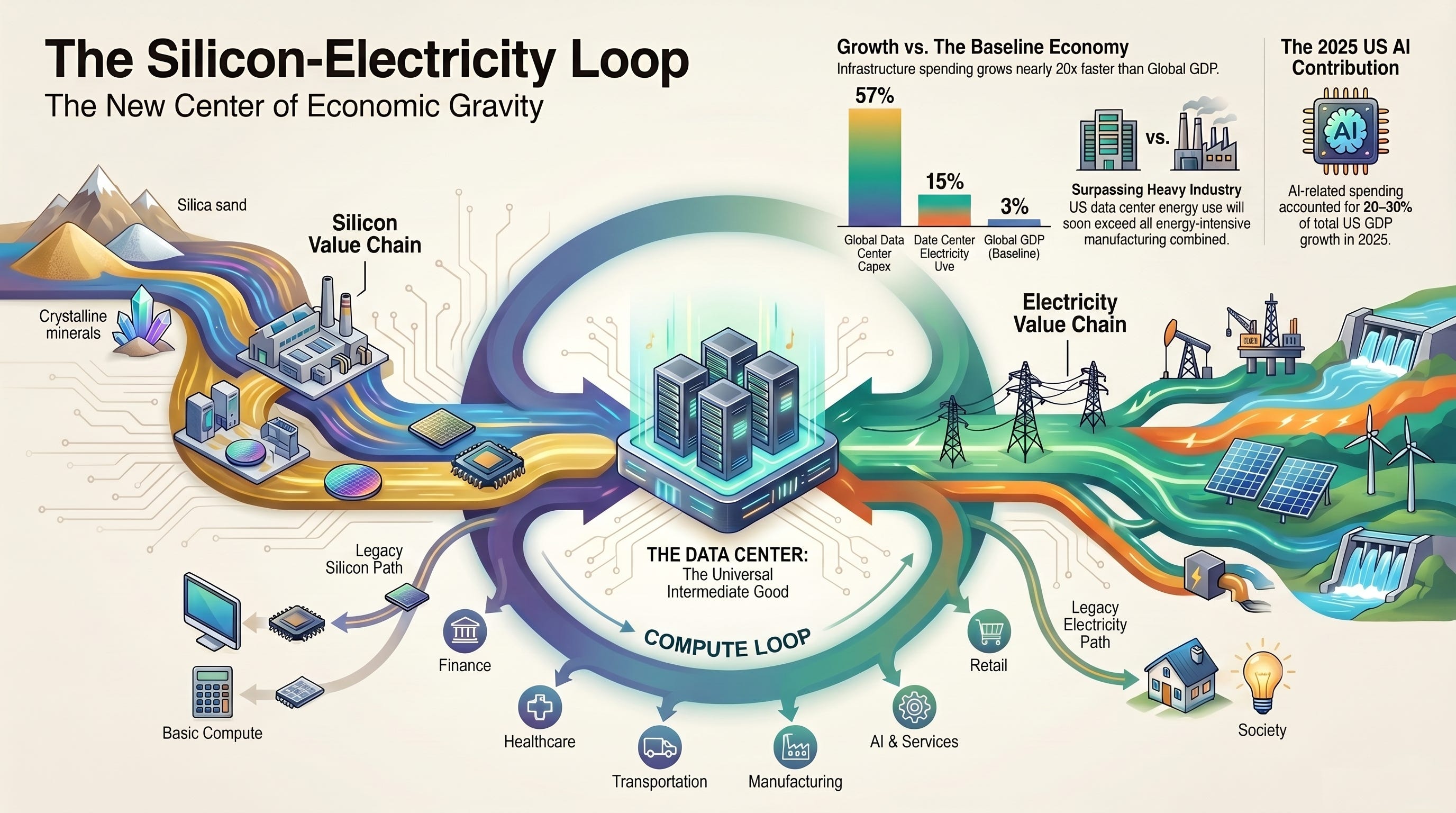

The dual silicon-electricity rail

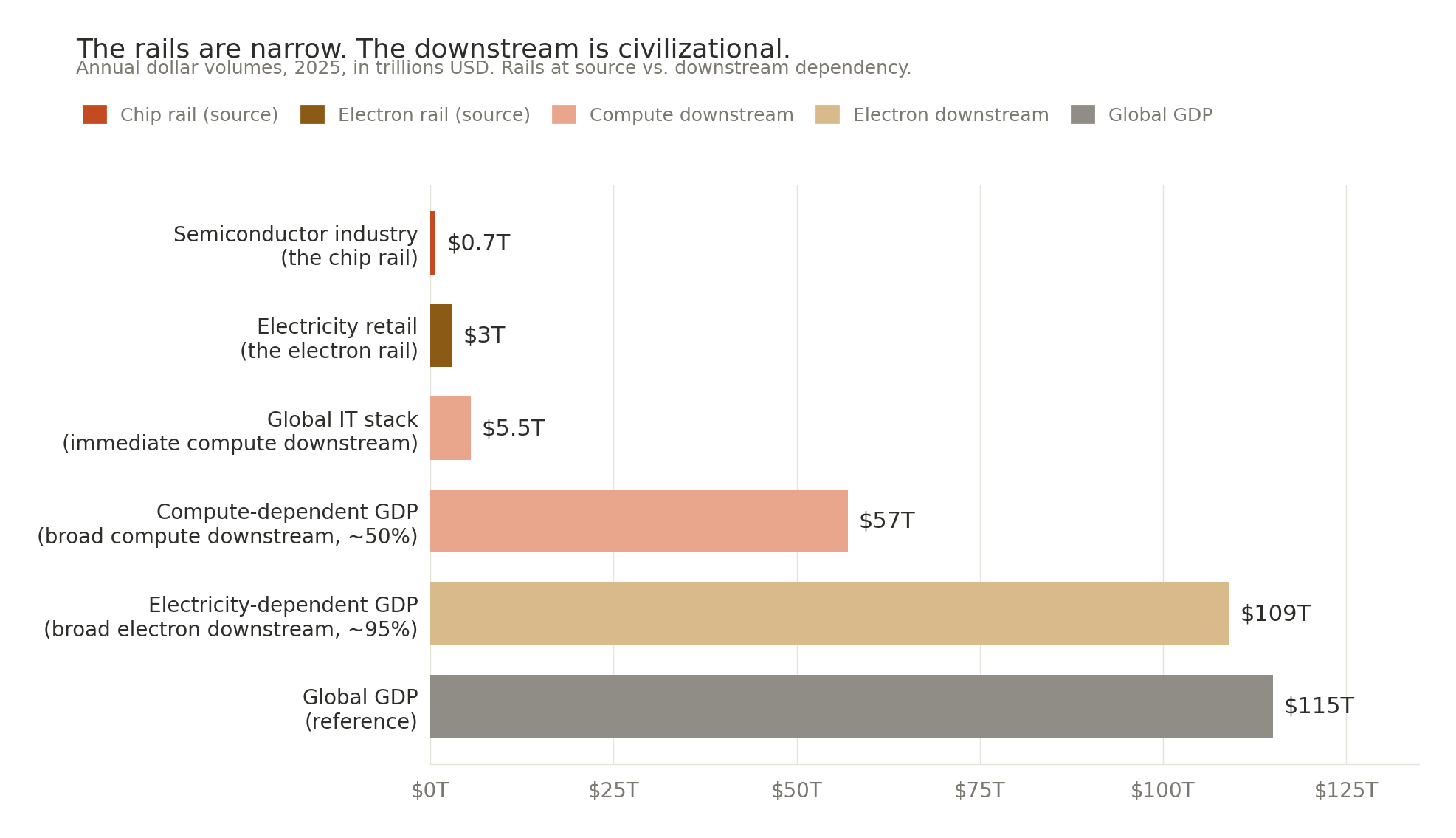

Two rails carry the modern economy: electrons and silicon.

Electricity moves $3 trillion in annual retail sales, and about 95% of global GDP sits downstream of it1. Microprocessors are a $700 billion industry with a $5.5 trillion IT stack riding on top of it (Gartner, 2025), and roughly half of global GDP is materially dependent on the outcomes.

These are not emerging sectors. They are civilizational plumbing. What is new is that both rails are being physically concentrated and rerouted into exactly one kind of ‘building’. The 2025 numbers:

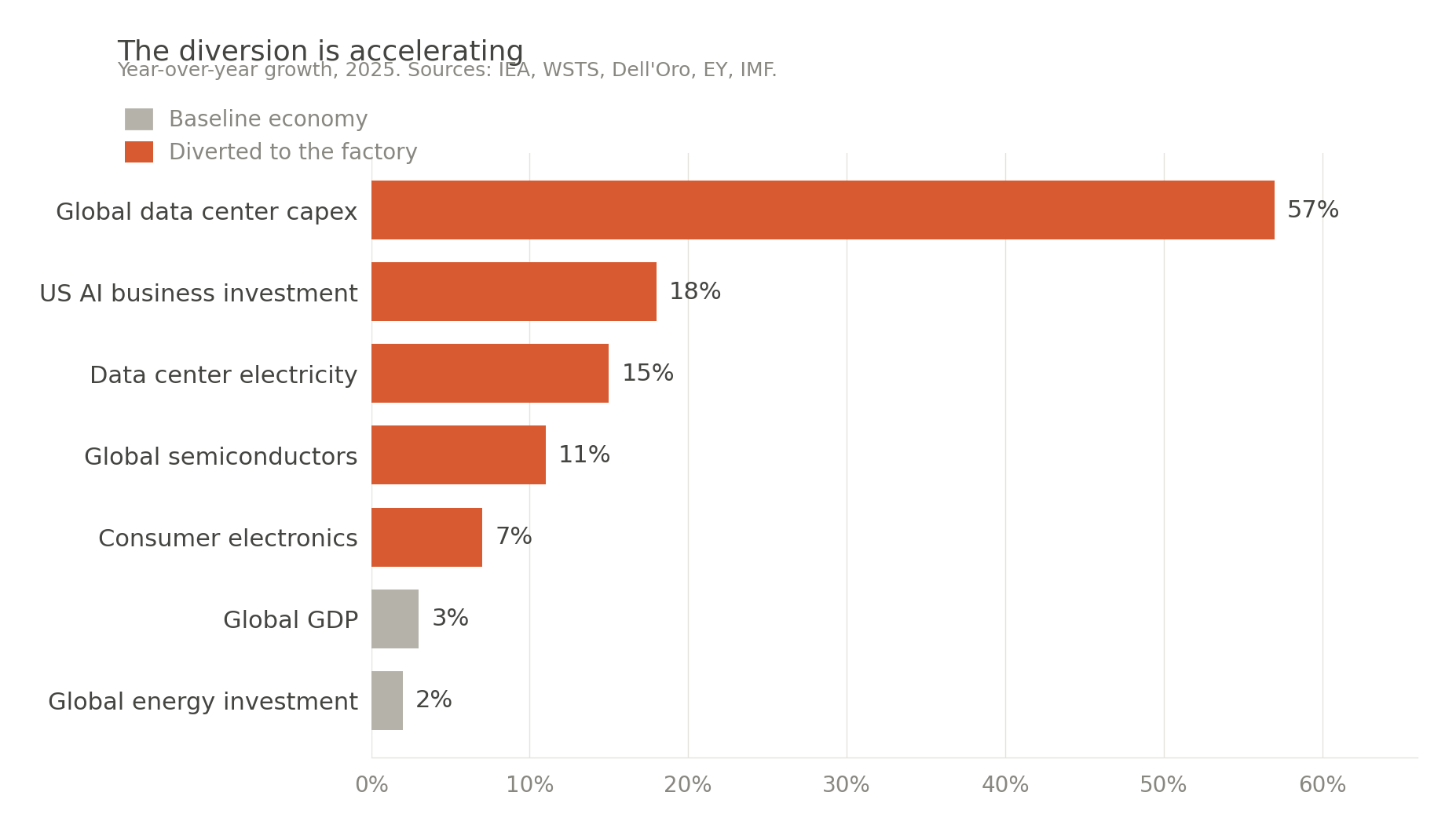

Data centers consumed about half of all US electricity demand growth (IEA).

Hyperscalers spent 45 to 57 cents of every revenue dollar on capex (J.P. Morgan; Dell’Oro).

Total data center buildout will reach $4 to $7 trillion through 2030 (McKinsey), what Jensen Huang (CEO, NVDA) has called the largest infrastructure program in human history

The rest of the economy grew at 3% (IMF); the rails feeding the data center grew 10 to 57% (WSTS, IEA, Dell’Oro)

That gap is not noise. It is an acceleration and a concentration.

The new factories of the LLM paradigm shift

The data center is becoming the factory of the 21st century, in the same structural role the Manchester mill played in the 19th century. The inputs are different (coal and cotton then, electrons and silicon now) but the pattern is identical: one kind of building, fed by the largest rails in the economy, producing a new intermediate good2.

That good is not compute. Compute was the old product. The new product is inference, delivered as agents, APIs, and embedded intelligence in every surface that used to be static. $7 trillion in capex is not insane once you understand you are not capitalizing more servers; you are capitalizing the birth of a new product category whose demand surface is every industry downstream of intelligence. From here, every large business sits in one of four positions:

Supplying silicon

Supplying electrons

Building the factory

Building on top of its output

Everyone else is a downstream customer.

Additional charts

🔍 Are you a builder or a technology leader?

Check out our book BUILDING ROCKETSHIPS 🚀 and continue this and other conversations in our 💬 ProductMind Slack community and our LinkedIn community.

Sources: IEA World Energy Investment 2025; WSTS / Semiconductor Industry Association; Gartner Worldwide IT Spending Forecast 2025; Mordor Intelligence Electricity Retail Market; McKinsey Global Institute; Dell’Oro Group; J.P. Morgan Asset Management; IMF World Economic Outlook; NVIDIA.

This part is not that surprising; we’ve been on this for more than a century.

In microeconomic terms, an intermediate good is a product or service used as an input in the production process to create other goods or services